Key takeaways:

- Record-low Bitcoin mining margins and rising demand for AI infrastructure incentivize miners to reduce their BTC positions.

- Institutional spot Bitcoin flows vastly surpass miner output, making macro trends more vital than miner profits alone.

Bitcoin’s price slide to $62,000 was paired with weak on-chain activity and declining BTC miner revenues, which have fallen to an all-time low. This revenue drop is fueling investor anxiety over potential sell pressure, especially since miners and mining pools still control over $110 billion in Bitcoin.

1 TH/second of hashing power per day returns, USD. Source: Luxor Hashrate Index

The estimated daily return for 1 terahash per second of hashing power plunged to an all-time low of $0.28 on Tuesday, down from $0.39 just a month ago. For context, the estimated monthly gross profit for an Antminer S21 XP Hydro (at an electricity cost of $0.07 per kilowatt-hour) has slid to $137, down from $192 last month.

This profitability crunch arrives as demand for AI capacity and infrastructure investments surged, dampening market sentiment just as the crucial $60,000 support level was put to the test.

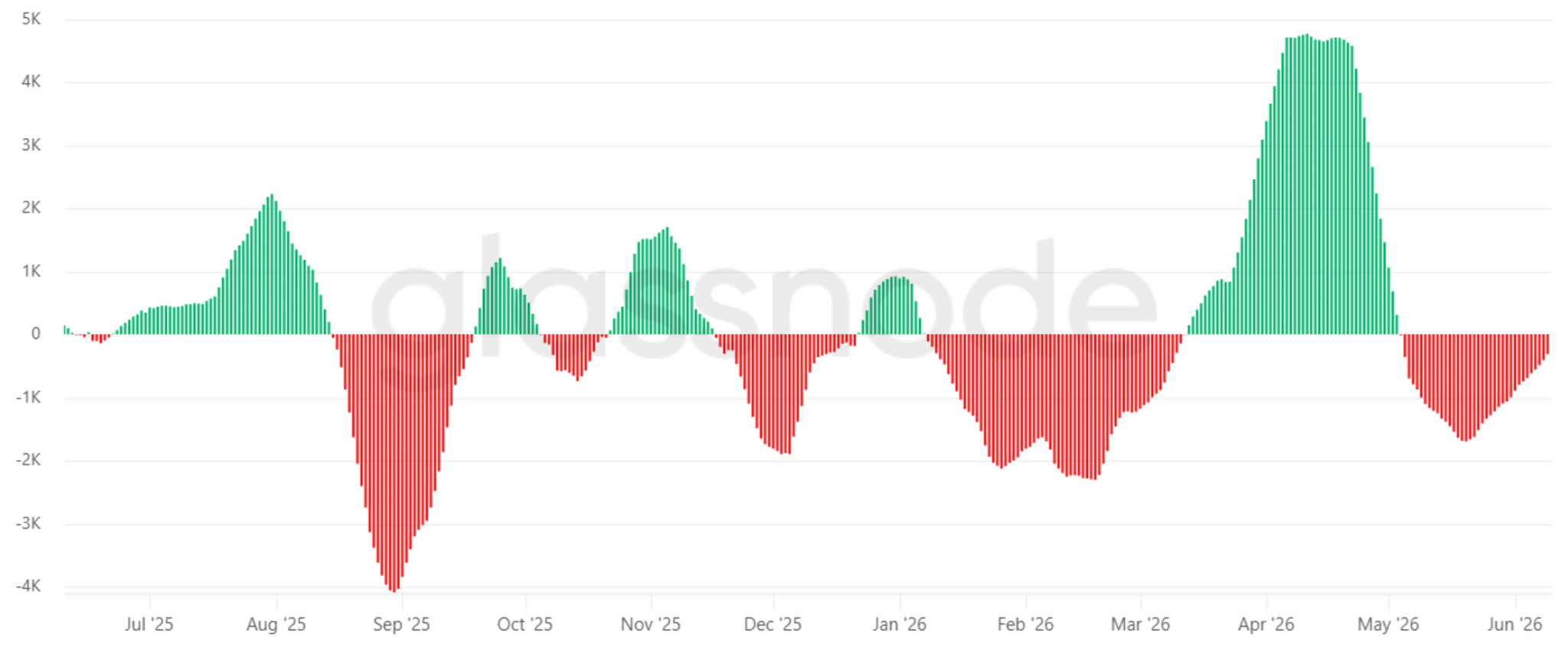

Bitcoin miners’ 30-day net position change, BTC. Source: Glassnode Studio

The 14-day average net position change for Bitcoin held in miner and mining pool addresses flipped negative in early May and has remained negative since. Whether these liquidations are intended to fund ongoing operations, reduce debt leverage, or bankroll expansion into AI data center computing, the net effect remains a heavy drag on Bitcoin’s price discovery.

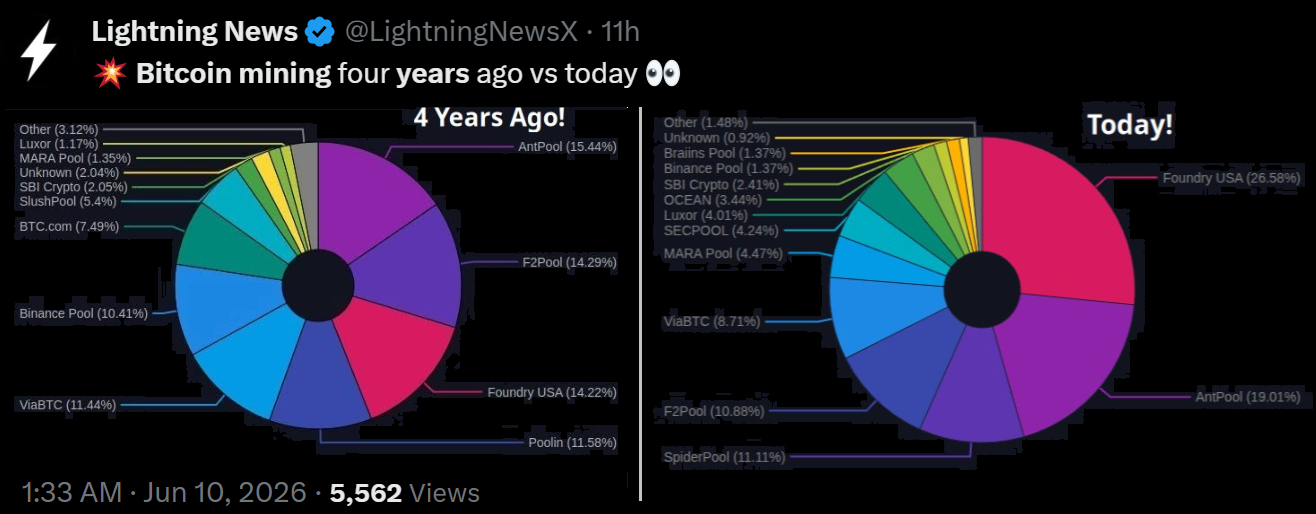

Source: X/LightningNewsX

The high concentration of Bitcoin hashrate among the three largest mining pools is a frequent target of analyst criticism. The latest 7-day data show that Foundry USA, AntPool, and F2Pool control a combined 59% market share. In contrast, the top three Bitcoin mining pools held a combined 44% hashrate market share back in 2022.

According to Bernstein analysts, the primary bottleneck for scaling AI data centers is access to electricity rather than chips. This constraint is prompting some Bitcoin miners to repurpose parts of their power infrastructure to support AI computing applications, a sector currently viewed as more stable and lucrative than traditional crypto mining.

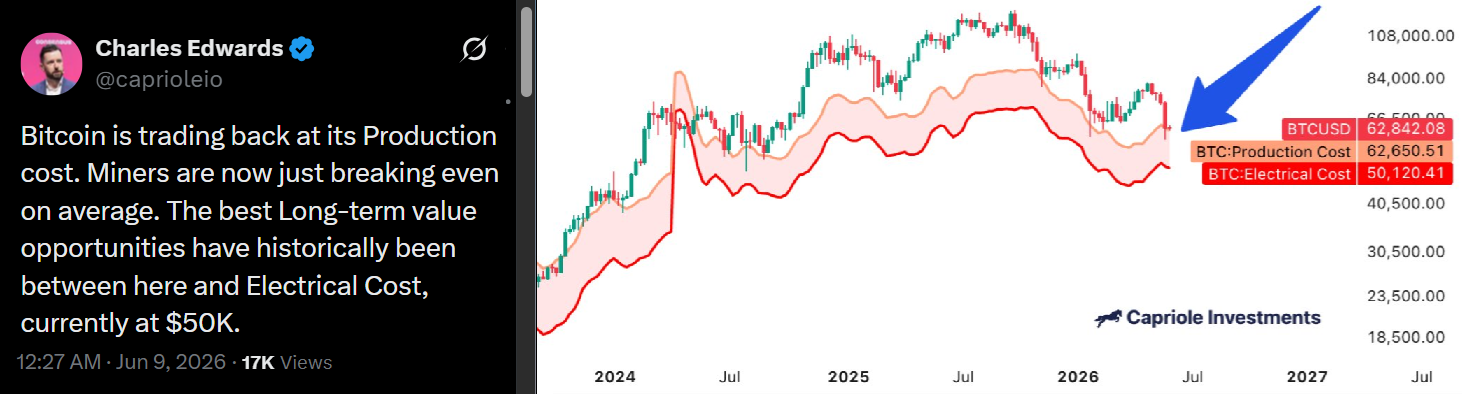

Source: X/Capriole Investments

According to Charles Edwards, founder of Capriole Investments, the Bitcoin mining production cost, including depreciation and amortization, stands at $62,650, while the absolute minimum to break even on electricity is $50,120. However, certain publicly listed companies leverage much more efficient ASIC models and industrial-scale energy contracts.

American Bitcoin Corp (ABTC US) reported gross operational costs near $36,200 per Bitcoin mined in the first quarter of 2026. Ultimately, pinning down a single, industry-wide production cost is impossible, and some operations choose to mine at a loss for specific tax benefits. Even if these high-cost miners temporarily shut down, spot institutional flows now vastly surpass miners’ output.

Related: Bitcoin may act as a ‘canary in the coal mine’ as risk-off pressure spreads–Bitwise

Bitcoin traded below its estimated production cost for more than six months in 2019 and again in 2023, based on Capriole Investments data. Whether the current market stagnation persists depends on investor risk perception amid broader macroeconomic uncertainty, rather than miner profitability alone.

Read the full article here